有人問我:

Q1, 台積電嘅自由現金流有下降趨勢, 唔係好事? (所以股價跌咁多?)

Q2, 台積電係咪講「大話」? 比市場識穿左? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

Q1, 台積電嘅自由現金流有下降趨勢, 唔係好事? (所以股價跌咁多?)

Q2, 台積電係咪講「大話」? 比市場識穿左? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

*********************************************************************************

喺答問題之前, 先帶大家睇睇 台積電 嘅收入組合

台積電嘅收入按製程分佈, 當中三成係7nm; 兩成係 5nm

兩者都可以話係"先進製程"

而佢地喺台積電嘅收入金額亦逾嚟逾高

由2019Q1 嘅 500億台幣, 到2022Q1 嘅 2455億台幣

技術平台嘅分佈

大約41% 係嚟自 高效能運算(HPC- High Performance Computing)

有40% 來自智慧型手機

大家記一記: 50% 7nm 5nm

41% 高效能運算(HPC- High Performance Computing)

*********************************************************************************

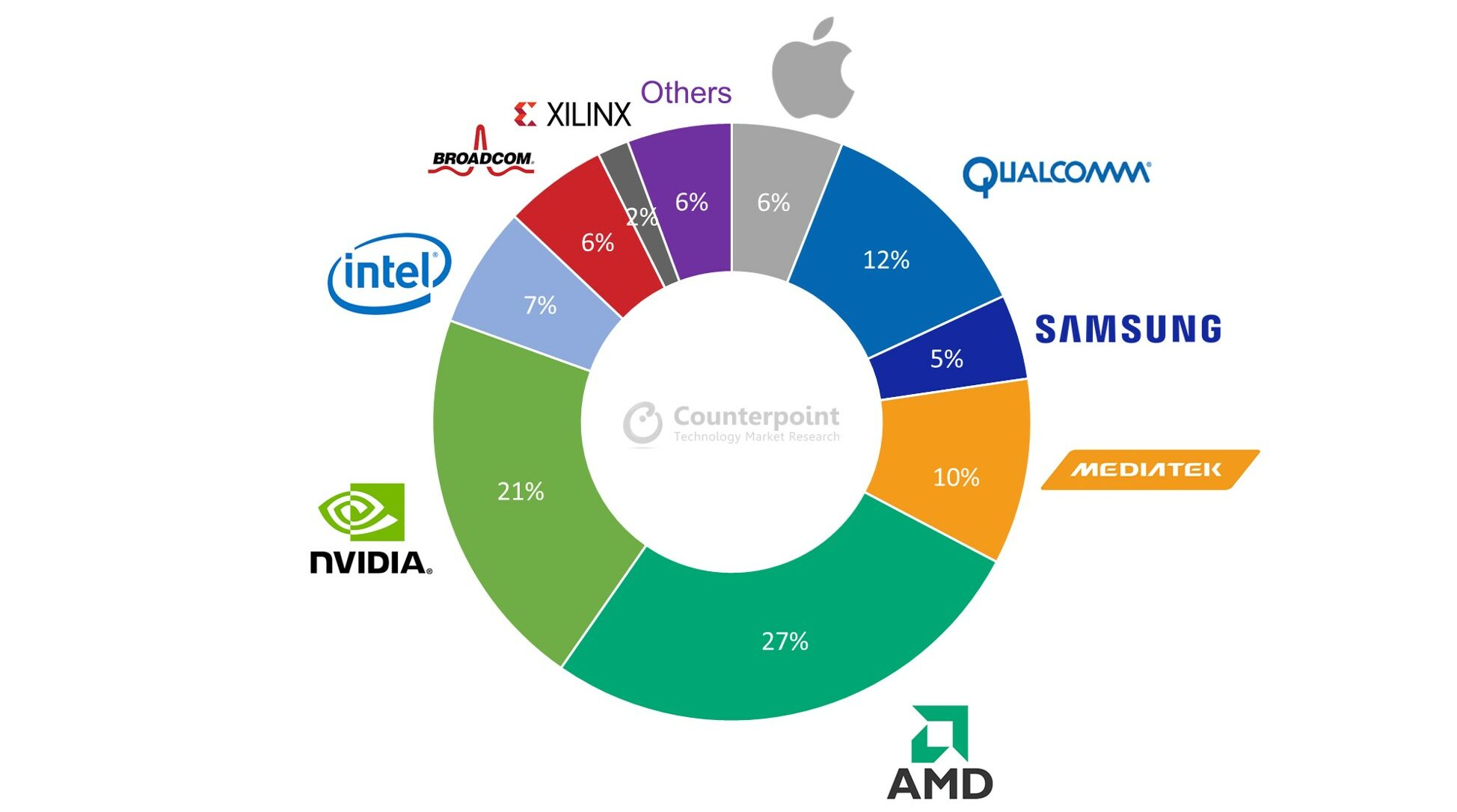

另外, 我地又睇下 台積電 嘅客戶:

|

| 7-nanometer (N7, N7+, N6) Wafer Shipment Breakdown by Customer, 2021 |

|

| 5-nanomater Wafer Shipment Breakdown by Customer, 2021 |

5nm 製程, 當中有53% 係Apple, 24% 係高通

7nm 製程, AMD佔27%, NVDA 佔21%

*********************************************************************************

關於Q1: 台積電嘅自由現金流有下降趨勢

首先要睇下 自由現金流 係咪真係跌?

跌嘅原因係點嚟?

首先要睇下 自由現金流 係咪真係跌?

跌嘅原因係點嚟?

(張圖有啲細) 我打返幾個items 出嚟先

項目: 2021年 (增幅%) 2020年 (增幅%) 2019年 (增幅%) 2018年

收入: $1587 (+18.5%) $1339 (+25.2%) $1069 (+3.7%) $1031

毛利率: 51.6% 53.1% 46% 48.3%

淨利率: 40.9% 42.3% 34.8% 37.2%

營運現金流: $1112 (+35.2%) $822 (+33.7%) $615 (+7.2%) $573

資本支出: $839 (+65.4%) $507 (+10.2%) $460 (+45.9%) $315

自由現金流: $272 (+13.5%) $315 (+103.9%) $154 (-40.1%) $258

自由現流/ 收入(%): 17% 23% 14% 25%

收入增幅非常靚仔

毛利率都有持續改善

純利率都係

營運現金流嘅增長比收入增幅大, 證明台積電嘅 固定資產投資係成功

可以「一本萬利」

向客戶加價, 同時亦向客戶收定錢先,

「想出貨先? 麻煩比多啲訂金」

最後, 自由現金流比率的確係下跌

點解呢? 營運現金流上升, 但自由現金流下跌

咁咪啫係 中間嘅「資本支出CAPEX」出事

出咩事? 咪就係capex大左

咁capex大左係咪壞事? 依個就係問題所在

capex 其實要再分 main capex & growth capex

前者係維持產能嘅資本支出

例如: 九巴公司, 本身有200架巴士, 每年有10架會壞而維修唔到, 要買返10架新巴士去替換

咁新嘅巴士就緊係用新價錢, 新價錢(通常)都會貴過上年

如果依類型嘅capex 增加, 要小心

成本增加同時, 要睇埋收入加唔加到

前題講左, 係替換舊嘅巴士, 載客量唔會多左, 咁啫係要睇九巴 有無得加價.

後者, Growth capex

就係九巴公司 本身有200架巴士, 佢再買多7架 去拓展新嘅巴士路線

乘客量會多左

返嚟台積電依到

大家有睇新聞都知, 佢去左美國建廠, 同時有唔同國家

而喺本身嘅計劃, 都要為更先進製程做科研&建廠 (2nm 3nm 5nm)

咁大家諗下, 依類型嘅CAPEX 增加, 兼且係大增, 係一件好事? 定壞定?

*********************************************************************************

Q2, 台積電係咪講「大話」? 比市場識穿左? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

首先, 我地要睇下台積電點講

喺2021年Q4 嘅業績會 (link)

Now I will move on to key messages. I will start by making some comments on our 2022 capital budget and depreciation. Every year, our capex is spent in anticipation of the growth that will follow in the future years. We are witnessing a structural increase in underlying semiconductor demand underpinned by the industry mega trends of 5G-related and HPC applications.In 2021, we spent USD 30 billion to capture the strong demand and support our customers' growth. In 2022, our capital budget is expected to be between USD 40 million to USD 44 billion. Out of the USD 40 billion to USD 44 billion capex for 2022, between 70% and 80% of the capital budget will be allocated for advanced process technologies, including 2-nanometer, 3-nanometer, 5-nanometer and 7-nanometer. About 10% will be spent for advanced packaging and mass making and 10% to 20% will be spent for specialty technologies.TSMC is working closely with our customers to plan our capacity and investing in leading-edge and specialty technology to support their group demand. At the same time, we are committed to achieve a sustainable and proper return that enable us to invest to support our customers' growth and deliver long-term profitable growth for our shareholders. Over the last three years, we have raised our capex spending from USD 14.9 billion in 2019 to USD 30 billion in 2021 as we invest in anticipation of the growth that will follow. During the same period, our revenue in US dollar term has increased from USD 34.6 billion in 2019 to USD 56.8 billion in 2021 or 1.6 times and our EPS by 1.7 times.We are continuing to work closely with our customer to support their growth, and our pricing strategy will remain strategic not optimistic to reflect our value creation. We will also work diligently in our own fab operation and with our suppliers to deliver on cost improvement. By taking such actions, we believe our long-term gross margin of 53% and higher is achievable, and we can earn a sustainable and proper return of greater than 25% ROE through that cycle. Thus, even as we shoulder a greater burden of capex investment for the industry, we can continue to invest to support our customers' growth and deliver long-term profitable growth for our shareholders.

台積電2021年Q4:

我地喺2022年嘅capex 有七成至八成係高效能運算(HPC), 2奈米 3奈米 5奈米 & 7奈米

我地同客戶緊密合作 (我地出capex 係有客戶需求先會去做)

(大家有無印像我最開段嘅收入分布?)

*********************************************************************************

喺2022年Q1 嘅業績會 (link)

Bruce, this is C.C. Wei. Let me answer your question. As you said, TSMC works closely with our customers to plain capacity. And our CapEx and capacity expansion plan are actually based on customers’ long-term demand profile, underpinned by the industry megatrend. We do not build capacity based on speculation. In advanced technology node, we have a leading position. In our mature node, our capacity is built to support customer demand for our differentiated specialty technologies. And we focus on building effective capacity, which is capacity that products and produce the specialized technology with high yield rather than just plain capacity. Thus, we are confident our capacity is built to support our customers’ growth, and our utilization and profitability will be sustained.Randy, this is C.C. Wei. Our CapEx and capacity expansion plan are always based on our customers’ long-term demand profile. This is underpinned by an industry megatrend. As long as the mega trend continues, which we believe it will, we will continue to invest to capture the growth that will follow. So even a short term with the possibility of downturn, which we don’t think it will impact too much to TSMC, if even it happens, we will continue our plan and we have confidence to invest to capture the growth that will follow.Krish, this is a tough question to be asked because we always in close working with our customers. So we know that each customer’s demand and their forecast and we plan our capacity, we plan our technology by working with them. So if there is a downturn, sure, we’ve got the first hand information from our customers. And we collect them together, and we do get it. And we decide our long-term CapEx and capacity. But which one is a leading indicator, that, I don’t have a specific answer for your questions.

btw..."C C Wei" 係人名呢, 佢係邊個? 台積電CEO

台積電2022年Q1:

我地同客戶緊密合作去計劃產能

我地嘅capex & 產能係建基於客戶嘅長期需求

我地喺增設產能嘅事情上, 唔係投機(賭)

就算短期有經濟下行, 我地相信對公司唔會有大影響

我地知道客戶嘅需求 & 佢地做嘅預測, 再去決定我地嘅產能(capex)

(大家有無印像我開段嘅客戶分布?)

*********************************************************************************

上面兩段喺業績講稿, 我相信可以解答

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

但! 上面兩段都係台積電講嘅

實有人會話, 可能台積電講大話呢?

well. 我真係笑撚左! 笑撚埋右

大家重溫下我之前寫嘅 NVDA 業績

當中提到:

Google: FY2022 Q1meaningful increase in Capex in 2022reflected in investments in Technical Infrastructure globallyGoogle: FY2021 Q4investment in our technical infrastructure, most notably in servers, to support ongoing growth in both Google Services and Google Cloudincrease in CapEx. In Technical Infrastructure, serversMSFT FY2022 Q2in the timing of our cloud infrastructureOur capital investments, including both new data centerAMZN FY2022 Q1just under 40% of that capex is going into infrastructure, most of it feeding AWS.AMZN FY2021 Q4About 40% of that went to infrastructure, primarily supporting AWSwe do expect infrastructure spend to grow year over year, in large part to support the rapid growth and innovation we're seeing within AWS.

三大科企 Google Microsoft Amazon 都提到嚟緊會加大投資喺雲相關嘅建設

當中包括運算 & 伺服器

側面證明 NVDA 喺未來嘅發展都唔會差得去邊

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

另外喺NVDA 嘅業績會講稿中提到:

Yes. So let me start here, and I'll see if Jensen wants to add more of that. Our purchase obligations, as well as our prepaid have two major things to keep in mind. One, for the first time ever, we are prepaying to make sure that we have that supply and those commitments long term.And additionally, on our purchase obligations, many of them are for long lead time items that are a must for us to procure to make sure that we have the products coming to market.A good percentage of our purchase commitments is for our Data Center business, which you can imagine, are much larger systems, much more complex systems and those things that we are procuring to make sure we can feed the demand both in the upcoming quarters and further. Areas in terms of where we are still a little bit supply constrained are networking. Our demand is quite strong.

Operating Cash flow 金額都跌左,主因係 prepaid expense

(同上年差唔多原因, 早啲比定錢TSMC & 其他供應商, 霸定生產線)

*********************************************************************************

三大雲服務巨頭都話要加capex 去發展雲業務

其實關咩事? 雲, 需要用到 data chip, 高效能運算(HPC- High Performance Computing)

(大家有無印像我最開段嘅收入分布?)

加多少少補充

喺前日, 另一個"雲"參與者出左業績發佈

甲骨文(ORCL)上季業績勝預期 CEO指雲基礎設施需求大幅增長集團行政總裁Safra Catz表示,看見了市場對雲基礎設施的需求大幅增長,並認為,這種收入增長的飆升表明其基礎設施業務現已進入高速增長階段。她表示,預計雲計算業務營收在2023財年第一季度將按年增長25%,在2023財年全年將(以固定匯率計算)按年增長30%。

而, 咁啱得咁"喬", 上面我quote 嘅台積電講: a structural increase in underlying semiconductor demand underpinned by the industry mega trends of 5G-related and HPC applications.

(大家有無印像我最開段嘅收入分布?)

同樣地, NVDA 都講到要確保未來嘅供應錶, 甚至要預付去霸好生產線

雖則同 台積電無必然關係

但至少可以肯定, 喺嚟緊嘅市場發展, 高效能運算(HPC)嘅晶片需求應該有加無減

*********************************************************************************

我地再睇下 台積電 另一個客點講

高通Qualcomm, 2022年Q2 季報: (link)

Long-term Capacity Commitments. We have entered into several, and we may enter into additional, multi-year capacity purchase commitments with certain suppliers of our integrated circuit products. In the first six months of fiscal 2022, we made $1.6 billion in advance payments related to certain obligations under these purchase agreements, which were included within other assets and other current assets at March 27, 2022. Additional information regarding long-term capacity commitments and other purchase obligations is provided in “Notes to Consolidated Financial Statements, Note 7. Commitments and Contingencies” in our 2021 Annual Report on Form 10-K.

2021Q4 年報: (link)

Purchase Obligations. We have agreements with suppliers and other parties to purchase inventory, other goods and services and long-lived assets. During fiscal 2021, we entered into several multi-year capacity purchase commitments with certain suppliers of our integrated circuit products. Integrated circuit product inventory obligations represent purchase commitments (including those under multi-year capacity purchase commitments to the extent such minimum amounts are both fixed and determinable) for raw materials, semiconductor die, finished goods and manufacturing services, such as wafer bump, probe, assembly and final test. Under our manufacturing relationships with our foundry suppliers and assembly and test service providers, cancellation of outstanding purchase commitments is generally allowed but may result in the payment of costs incurred through the date of cancellation, and in some cases, incremental fees and/or the loss of amounts paid in advance related to capacity underutilization and the failure to meet future minimum purchase volumes under multi-year capacity purchase commitments. Obligations under our purchase agreements, which primarily relate to integrated circuit product inventory obligations, at September 26, 2021 totaled $23.5 billion of which, $12.9 billion is expected to be paid in the next 12 months.

高通係講:

我地有幾年嘅購貨協議, 關於晶片供應

我地有預付依啲嘅購貨協議

依啲購貨協議係可以取消, 但會有相應嘅損失

上面係關於向晶片制造商購買產能,

以下係 QCOM 對於未來嘅睇法:

Cristiano Amon; President and CEOThank you, Mauricio, and good afternoon, everyone. Thanks for joining us today. As the pace of digital transformation of industries accelerates and as devices become connected and more intelligent, our broad portfolio of technologies and solutions is creating a significant long-term growth opportunity for us.

簡單一個字, 前景好!

*********************************************************************************

睇完未? 落得定論未? 未! 不到黃河心不死!

我地睇埋 台積電嘅其中一個競爭對手 三星 Samsung

搵左編報導: (link)

韓媒etnews報導,三星的晶圓事業已拿到未來5年200兆韓元(約5.09兆台幣)訂單,若能完成3奈米製程確認並在第2季啟動量產,預計能獲得更多訂單。三星強調,先前存在良率問題的4.5奈米製程,已趨於穩定。報導指出,三星晶圓部門副總裁Moon-soo Kang上周在發布第1季財報的法說會上表示:「未來5年的剩餘訂單是去年營收的8倍,這個數字只會增加。」基於界內估計三星去年晶圓代工營收介於23至25兆韓元,「剩餘訂單」價值推估上看200兆韓元。三星晶圓事業強調,已確保直到2027年的供應。

台積電嘅競爭對手三星: 收入增長, 營收8倍 (成個市場都增長好勁)

台積電嘅競爭對手三星: 產能去到2027

如果台積電做左傻仔, 第日會產能過剩, 咁三星都一樣會係傻仔

地球上兩大晶片代工巨頭都會做傻仔?

*********************************************************************************

睇多間競爭對手 (link)

|

| 格羅方德 (GFS) Corporate Overview Presentation, May 3, 2022 |

另一間晶片製造商 格羅方德GlobalFoundries (GFS)

佢喺今年5月份, 其中一張Power Point 提到, 成個晶片行業 & 代工行業 未來5年嘅市場規模

年複合增長分別為: 8.2% 9.8%

問題嚟啦,

跟據2021年嘅市場份額(link),

台積電佔53%; 三星18% ; Global Foundries 6%

晶片代工三巨頭 都會預計市場未來係向好嘅

唔通, 三個巨頭都係傻仔? (一定係, 除非唔係)

Q2, 台積電係咪講「大話」? 比市場識穿左? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

*********************************************************************************

真係最後

睇埋 台積電嘅供應商, 亦係晶片界最終玩家: ASML, 光刻機製造商

|

| ASML 2021年報 Page 28 |

|

| statista 圖像化ASML 預測 |

ASML 預計緊去到2025年 嘅市場年複合增長為8.2%

*********************************************************************************

完, 真係完, I mean 睇資料嘅部份

去返最開頭嘅問題先:

Q1, 台積電嘅自由現金流有下降趨勢, 唔係好事? (所以股價跌咁多?)

Q2, 台積電係咪講「大話」? 比市場識穿左? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

Q2, 台積電係咪講「大話」? 比市場識穿左? (所以股價跌咁多?)

Q3, 台積電嚟緊幾年會唔會產能過剩? (所以股價跌咁多?)

A1, 自由現金流的確有下降, 相信同擴大產能有關

A2, 台積電 有無講大話, 我就真係唔知

但世界頭30市值嘅公司一齊講大話, 我就真係笑撚左! 笑撚埋右

|

| dogsofthedow |

A3, 未來係咪會產能過剩, 我都係唔知嘅. 無水晶球 亦無時光機

但整體需求向上亦係成個行業參與者嘅預測

咁可能成個行業一齊睇錯市

學某人話齋, 大過0% 都係有可能

近排我見到有個Facebook Page 講嘅野好啱, 大家一齊睇下

今日篇野, 同大家一齊尋寶

未來點發生無人知

但

成個市場一齊講大話?

成個市場一齊做傻仔?

well... 睇年報 睇數簿

唔好自亂陣腳

唔好股價跌就9up搵理由

唔好股價跌就話公司管理層講大話...

-完-

*********************************************************************************

🔴🔴🔴Patreon: 台積電 TSM 估值 (2022 Apr)

🔴🔴🔴Patreon: Nvidia NVDA 估值 (2022 May)

🟩🟩🟩台積電 TSM 2022Q1 第1季 業績

🟩🟩🟩Nvidia NVDA 2023年度 第1季業績

🟡🟡🟡Google 業績

🟡🟡🟡Microsoft 業績

🔴🔴🔴Patreon支持: 港股美股英股估值

🟡🟡🟡YouTube Channel

🟠🟠🟠Blog: 業績分析, 會計技巧

🟦🟦🟦Facebook Page

🟩🟩🟩若果寫嘅野幫到你, 請我飲咖啡? PayMe!

📩📩📩 DKLM10PM@Gmail.com

*********************************************************************************

50 Largest Companies by Market Cap Toda

Foundry Industry’s Robust Revenue Growth to Continue in 2021

三星斥晶圓代工能見度不清 自曝200兆韓元訂單到手!

台積電幾乎滿單到2024年

TSMC, Taiwan to increase foundry market share in 2022

好似做記者咁做資料搜集

回覆刪除謝謝詳細分享

回覆刪除Thank for the information.

回覆刪除